In today’s fast-paced digital age, the financial industry has witnessed a significant transformation, with online banking emerging as a cornerstone of modern finance. As technology continues to evolve, so does the landscape of online banking. In this article, we will delve into the future of online banking and highlight the key trends that are poised to reshape the way we manage our finances.

The Rise of Digital-First Banks

In the ever-evolving landscape of online banking, one trend that has been gaining significant momentum is the rise of digital-first banks. These innovative financial institutions are redefining the way we think about traditional banking by operating exclusively through digital channels. The digital-first banking model not only offers a refreshing departure from brick-and-mortar branches but also comes with a host of advantages that are reshaping the financial industry.

A Digital-First Approach

Digital-first banks, often referred to as neobanks or challenger banks, are built from the ground up with a digital-first mindset. Unlike traditional banks with physical branches, these institutions have no physical presence, allowing them to significantly reduce overhead costs. This cost efficiency translates into tangible benefits for customers in the form of higher interest rates on savings accounts and reduced fees for various services.

Streamlined Account Setup

One of the key attractions of digital-first banks is the ease and speed with which customers can open accounts. Traditional banks typically require individuals to visit a branch in person, fill out paperwork, and provide multiple forms of identification. In contrast, digital-first banks enable users to complete the entire account setup process online, often within minutes. All that’s needed is a smartphone or computer with an internet connection.

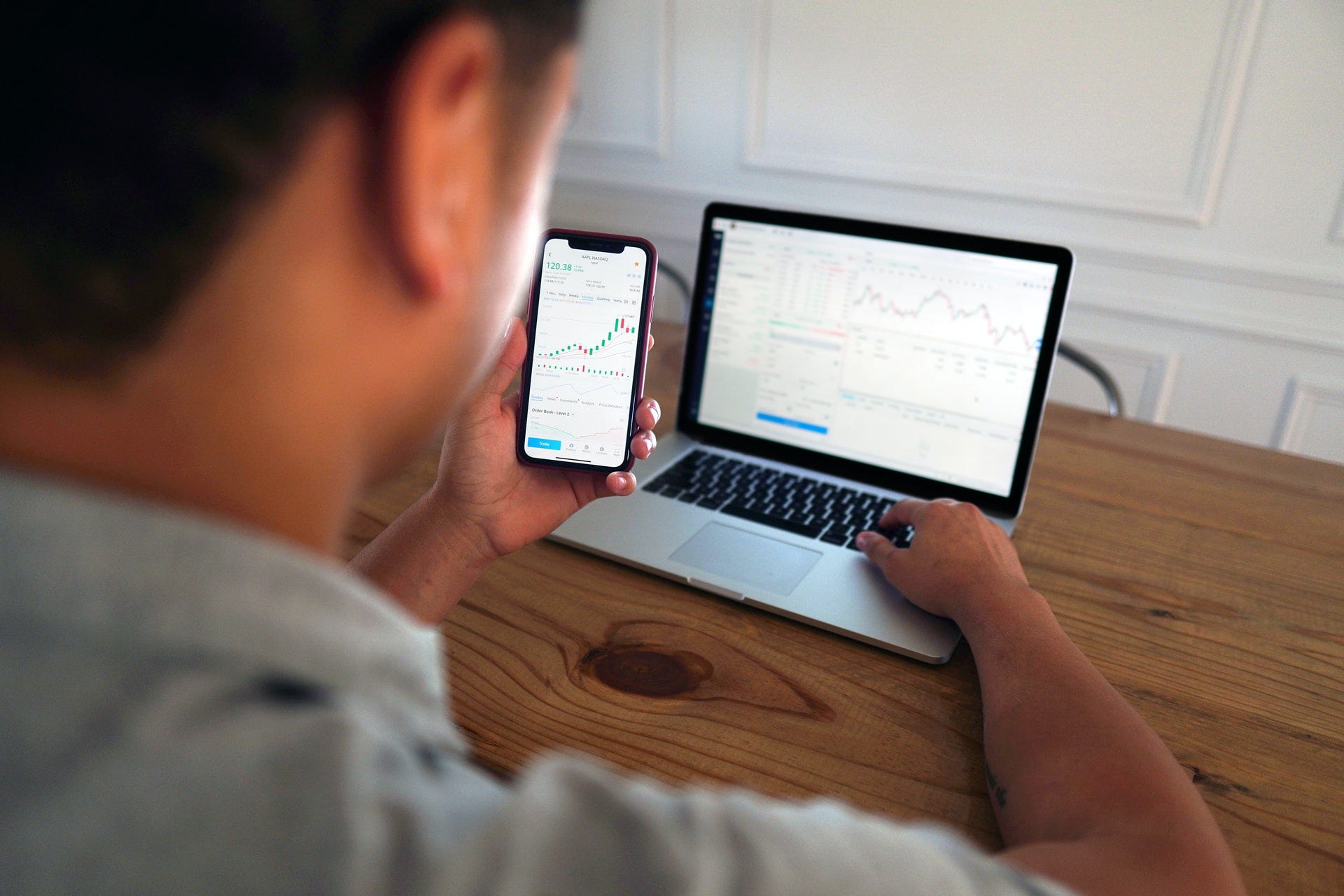

Mobile-Centric Banking

Mobile banking is at the heart of the digital-first banking experience. These banks prioritize mobile app development to provide customers with seamless access to their accounts, transactions, and financial management tools. The mobile apps are designed with user-friendly interfaces, intuitive navigation, and real-time updates, ensuring that customers can easily manage their finances on the go.

Enhanced Customer Experience

Digital-first banks place a strong emphasis on customer experience. Since they rely solely on digital interactions, providing excellent customer service through online channels is paramount. Many of these banks leverage technology, such as AI-driven chatbots, to offer quick responses to customer inquiries, resolve issues, and even provide financial advice, all in real-time.

Global Accessibility

Another notable feature of digital-first banks is their global accessibility. Traditional banks often have limited international reach, which can be a significant inconvenience for individuals who frequently travel or conduct business across borders. Digital-first banks, on the other hand, often provide accounts with features specifically designed for international use, such as fee-free currency conversion and international money transfers at competitive rates.

Personal Finance Management

These banks aren’t just about basic banking services; they aim to empower users with advanced personal finance management tools. Through data analytics, they can offer tailored recommendations for budgeting, saving, and investing based on individual spending patterns. This level of personalization helps customers make more informed financial decisions.

Enhanced User Experience

In the fast-paced world of online banking, user experience (UX) has become a paramount concern for both financial institutions and their customers. The continued evolution of technology has given rise to heightened expectations regarding the ease, accessibility, and overall satisfaction of digital banking interactions. In this section, we will explore how online banks are enhancing user experiences to create more seamless and customer-centric financial services.

Intuitive User Interfaces

One of the fundamental aspects of improving user experience in online banking is the creation of intuitive user interfaces (UI). Online banks are investing significantly in designing UIs that are user-friendly and easy to navigate. The goal is to minimize the learning curve for customers and make it effortless for them to access their accounts, check balances, transfer funds, and perform other essential banking tasks.

Mobile-First Design

With the prevalence of smartphones, a mobile-first approach has become essential for delivering exceptional user experiences. Online banks prioritize the development of mobile apps that offer all the functionality of their desktop counterparts. These apps are optimized for various screen sizes and provide consistent and smooth experiences across devices.

Real-Time Updates

Customers today expect real-time updates on their financial transactions and account balances. Online banks have risen to the challenge by providing immediate feedback and notifications. Whether it’s receiving an alert for a credit card transaction or tracking the progress of a fund transfer, customers can stay informed at all times, enhancing their confidence in online banking.

Personalization

Personalization is a key driver of improved user experiences. Online banks utilize customer data and artificial intelligence to offer personalized recommendations and insights. For instance, they can suggest budgeting strategies based on spending patterns, recommend suitable investment options, or provide alerts for upcoming bills. This level of personalization not only improves customer satisfaction but also empowers individuals to make better financial decisions.

Enhanced Security Measures

While convenience is crucial, so is security. Online banks are continually enhancing their security measures to protect customer data and financial transactions. Advanced encryption techniques, multi-factor authentication, and real-time fraud detection systems are becoming standard features. Customers can feel confident that their financial information is safe while enjoying a smooth user experience.

Accessibility Features

Online banks are also prioritizing accessibility features to ensure that all customers, including those with disabilities, can use their services. This includes features like screen readers, voice commands, and simplified navigation options. Accessibility improvements not only demonstrate inclusivity but also expand the potential customer base.

Continuous Feedback Loop

To maintain and improve user experiences, online banks actively seek feedback from their customers. They encourage users to provide input on their banking experiences, identify pain points, and suggest enhancements. This feedback loop allows banks to make iterative improvements and tailor their services to meet customer expectations.

Artificial Intelligence and Chatbots

The integration of artificial intelligence (AI) and chatbots into the world of online banking has ushered in a new era of customer service and engagement. These technologies are revolutionizing how financial institutions interact with their customers, providing faster responses, greater accessibility, and a more personalized experience. In this section, we will delve into the impact of AI and chatbots on the online banking landscape.

Rapid Responses and Availability

One of the most noticeable advantages of AI-driven chatbots is their ability to provide rapid responses and be available around the clock. Unlike human customer service representatives who have limited working hours, chatbots can instantly address customer queries, 24/7. Whether a customer needs to check their balance, inquire about recent transactions, or report a lost card, chatbots are there to assist in real-time.

Enhanced Customer Engagement

AI-powered chatbots are more than just automated response systems. They are designed to engage customers in meaningful conversations. By analyzing customer inquiries and transaction history, chatbots can offer personalized recommendations, such as suggesting suitable financial products, explaining investment options, or helping users create a budget. This level of engagement goes beyond basic assistance and adds value to the customer experience.

Continuous Learning and Improvement

Chatbots equipped with machine learning capabilities continuously improve their performance. They learn from each interaction, gaining a better understanding of customer preferences and needs over time. This learning process allows them to provide increasingly accurate responses and anticipate customer queries, further enhancing the user experience.

Accessibility and Convenience

AI-driven chatbots make online banking more accessible and convenient for everyone. Customers can interact with chatbots through various channels, including web chat, mobile apps, and even voice assistants. This versatility ensures that users can access banking services in the way that suits them best, whether they prefer typing their queries or speaking them aloud.

Handling Complex Tasks

Modern chatbots are not limited to handling basic queries; they can also assist with more complex tasks. For instance, they can guide customers through the process of opening a new account, help with mortgage applications, or provide investment advice based on financial goals and risk tolerance. This versatility makes chatbots valuable resources for customers seeking comprehensive banking services.

Improved Efficiency

AI-driven chatbots significantly improve operational efficiency for banks. They can handle a high volume of inquiries simultaneously without the need for additional staffing. This not only reduces operational costs but also ensures that customers do not have to wait in long queues or on hold when seeking assistance.

Data-Driven Insights

Chatbots play a crucial role in collecting valuable customer data. By analyzing these interactions, banks can gain insights into customer preferences, pain points, and trends. This data-driven approach enables banks to make informed decisions about product development, marketing strategies, and overall service improvement.

Biometric Authentication

In the realm of online banking, security is paramount. As financial transactions and sensitive data move into the digital space, the need for robust authentication methods has never been greater. Biometric authentication has emerged as a cutting-edge solution that not only enhances security but also provides a more convenient and user-friendly experience for customers. In this section, we will explore the world of biometric authentication in online banking.

A Revolution in Security

Traditional authentication methods, such as passwords and PINs, have their limitations. They can be forgotten, guessed, or stolen. Biometric authentication addresses these vulnerabilities by relying on unique physical or behavioral characteristics of individuals. These characteristics, including fingerprints, facial features, and even voice patterns, are difficult to replicate, making them exceptionally secure.

Fingerprint Recognition

Fingerprint recognition is one of the most widely adopted forms of biometric authentication in online banking. The process involves scanning a user’s fingerprint and comparing it to a stored template. If there is a match, the user is granted access. The use of fingerprint recognition not only enhances security but also streamlines the login process, eliminating the need to remember complex passwords.

Facial Recognition

Facial recognition technology is becoming increasingly prevalent in online banking apps and systems. It works by analyzing unique facial features, such as the arrangement of eyes, nose, and mouth, to verify a user’s identity. The user simply needs to look into their device’s camera to gain access. Facial recognition offers a high level of security while providing a seamless user experience.

Voice Recognition

Voice recognition is another biometric authentication method gaining traction in online banking. It assesses the unique vocal characteristics of an individual, such as pitch, tone, and speech patterns. Users can simply speak a passphrase or provide a voice sample for verification. Voice recognition adds an additional layer of security without requiring any physical contact.

Iris and Retina Scanning

Iris and retina scanning are highly advanced biometric authentication methods that have found applications in some online banking systems. These techniques involve scanning the patterns in the user’s iris or retina, which are unique to each person. While less common than other biometric methods, they offer exceptional security and accuracy.

Enhanced User Experience

Beyond the security benefits, biometric authentication significantly enhances the user experience in online banking. Customers no longer need to remember multiple passwords or PINs, reducing the risk of forgotten credentials. The authentication process is also quick and convenient, aligning with the demands of today’s fast-paced digital world.

Multifactor Authentication

Many online banks employ multifactor authentication, combining biometric methods with other forms of verification, such as one-time passwords (OTPs) sent via SMS or email. This layered approach further strengthens security, ensuring that even if one factor is compromised, there are additional layers of protection in place.

Personalized Financial Services

The future of online banking is not just about accessibility and convenience; it’s also about personalization. Online banks are leveraging data analytics and artificial intelligence (AI) to offer personalized financial services that cater to individual needs and preferences. In this section, we will explore how personalized financial services are reshaping the way customers manage their money.

Data-Driven Insights

One of the cornerstones of personalized financial services is the use of data-driven insights. Online banks gather a wealth of data about customer transactions, spending patterns, savings goals, and more. By analyzing this data, banks can gain valuable insights into each customer’s financial behavior.

Tailored Recommendations

With the insights gathered, online banks can provide tailored recommendations to their customers. For example, if a customer frequently dines out, the bank’s app might suggest budgeting strategies for dining expenses or recommend credit cards that offer cashback rewards on restaurant spending.

Investment Guidance

Personalized financial services extend to investment guidance as well. Using data on risk tolerance, investment goals, and time horizons, online banks can recommend investment portfolios that align with each customer’s financial objectives. This level of guidance can help customers make informed investment decisions.

Savings and Budgeting

Many online banks offer features that help customers save and budget more effectively. They can analyze spending habits and identify areas where customers can cut costs or increase savings. This proactive approach to financial management encourages better money habits.

Alerts and Notifications

To keep customers informed and engaged, online banks send personalized alerts and notifications. These can range from reminders to pay bills, updates on account balances, and even alerts about unusual or suspicious transactions. Customers have the flexibility to set these alerts based on their preferences.

Financial Planning Tools

Online banks often provide financial planning tools that allow customers to set savings goals, track progress, and visualize their financial future. These tools can factor in variables like income, expenses, investments, and even life events to help customers make long-term financial plans.

Credit Management

Understanding the importance of credit, some online banks offer personalized credit management services. They can provide tips on improving credit scores, suggest credit card options, and even offer credit monitoring to protect against identity theft.

Customer Engagement

Personalized financial services enhance customer engagement by demonstrating that the bank cares about each customer’s financial well-being. These services create a more meaningful and interactive relationship between the bank and its customers.

Privacy and Data Security

While personalized financial services rely on data analysis, privacy and data security remain paramount. Online banks must ensure that customer data is protected and used responsibly. Stringent security measures and compliance with data protection regulations are crucial in this regard.

Open Banking and Collaboration

In the dynamic landscape of online banking, the concept of open banking and collaboration has emerged as a transformative force. It represents a fundamental shift from traditional banking models by encouraging financial institutions to partner with fintech companies and share customer data securely. In this section, we will explore the significance of open banking and collaboration in the future of online banking.

What Is Open Banking?

Open banking is a framework that allows customers to share their financial data securely with authorized third-party providers. These providers can include fintech startups, app developers, and other financial institutions. The goal is to foster competition, innovation, and greater choice for customers while maintaining robust security measures.

Improved Customer Experiences

One of the primary benefits of open banking is the potential for improved customer experiences. By sharing financial data with third-party providers, customers can access a wider range of financial services and tools within a single app or platform. For example, a customer could view accounts from multiple banks in a single dashboard, track spending, and manage investments, all in one place.

Access to Innovative Services

Open banking encourages collaboration between traditional banks and fintech companies, leading to the development of innovative services and products. Fintech startups often specialize in areas like budgeting apps, investment platforms, or loan marketplaces. Through partnerships, traditional banks can offer their customers access to these cutting-edge solutions.

Streamlined Financial Management

Open banking also simplifies financial management. Customers no longer need to switch between multiple banking apps or websites to access different accounts or services. This unified approach makes it easier to track finances, pay bills, and make informed financial decisions.

Enhanced Competition

Open banking fosters healthy competition within the financial industry. Traditional banks are incentivized to improve their services and offer competitive rates to retain customers. Meanwhile, fintech startups have the opportunity to reach a broader audience through established banking partnerships.

Security and Data Privacy

While open banking involves sharing financial data, security and data privacy are paramount. Stringent security measures and data protection regulations, such as the European Union’s General Data Protection Regulation (GDPR), ensure that customer data is handled securely and only used for authorized purposes.

The Role of APIs

Application Programming Interfaces (APIs) play a crucial role in enabling open banking. Banks provide APIs that allow third-party providers to access customer data, with the customer’s explicit consent. These APIs ensure that data sharing is secure, controlled, and compliant with regulations.

Customer Empowerment

Open banking puts customers in the driver’s seat, allowing them to decide which third-party providers can access their data. Customers have the power to grant and revoke access, providing them with greater control over their financial information.

Blockchain Technology in Banking

Blockchain technology, originally developed to underpin cryptocurrencies like Bitcoin, has found its way into the heart of the banking industry. This revolutionary technology is poised to transform the way banks conduct transactions, manage records, and enhance security. In this section, we will explore the significance of blockchain technology in banking and the various ways it is reshaping the industry.

Transparency and Security

One of the primary advantages of blockchain technology in banking is its unparalleled transparency and security. A blockchain is essentially a distributed ledger that records transactions across a network of computers. Each transaction is encrypted, time-stamped, and linked to the previous one, forming a chain of data blocks. This makes it nearly impossible for anyone to alter past transactions without altering all subsequent ones, ensuring the integrity of the ledger.

Faster and Cost-Effective Transactions

Blockchain technology has the potential to significantly reduce the time and cost associated with cross-border transactions. In traditional banking, international transfers often involve multiple intermediaries, each adding delays and fees. Blockchain can streamline this process by enabling direct peer-to-peer transfers across borders, making transactions faster and more cost-effective.

Smart Contracts

Smart contracts, a core feature of blockchain technology, are self-executing contracts with predefined rules and conditions. These contracts automatically execute and enforce themselves when the specified conditions are met. In banking, smart contracts can streamline processes like loan origination, trade finance, and insurance claims, reducing paperwork, delays, and the risk of disputes.

Improved Identity Verification

Blockchain technology can enhance identity verification and customer onboarding processes. With blockchain-based identity verification, customers can have a secure digital identity that they control. Banks can access this identity, simplifying the onboarding process while maintaining the highest standards of security and privacy.

Cross-Border Payments

Blockchain’s borderless nature makes it ideal for cross-border payments. International transactions can be settled in real-time, eliminating the need for correspondent banks and reducing the risk of delays and errors. This has the potential to revolutionize the global payments infrastructure.

Digital Assets and Tokenization

Blockchain enables the creation and management of digital assets and tokenized assets. This can include representing traditional assets like real estate or stocks as digital tokens on a blockchain. Banks can offer customers the ability to invest in and trade these digital assets, unlocking new investment opportunities.

Regulatory Compliance

Blockchain technology can assist banks in meeting regulatory requirements. Transaction data on a blockchain is immutable and can be easily audited, simplifying compliance efforts. Additionally, blockchain can facilitate Know Your Customer (KYC) and Anti-Money Laundering (AML) procedures by securely storing and sharing customer identity data.

Interbank Settlements

Blockchain consortia, where multiple banks join forces on a shared blockchain network, can streamline interbank settlements. This collaborative approach can reduce settlement times, lower costs, and enhance transparency among participating banks.

Cybersecurity Measures

In the rapidly evolving landscape of online banking, robust cybersecurity measures are of paramount importance. Banks employ advanced encryption methods, real-time monitoring, and threat detection systems to protect customer data and financial assets. These measures ensure the safety and integrity of online banking transactions and accounts, instilling trust and confidence in customers. As cyber threats continue to evolve, banks remain vigilant in adapting and strengthening their cybersecurity defenses to stay one step ahead of potential risks and attacks.

Green Banking Initiatives

In response to growing environmental concerns, green banking initiatives are gaining momentum within the financial industry. These initiatives involve investments in environmentally responsible projects and support for sustainable businesses. Green banks aim to align financial services with eco-conscious consumers, promoting sustainability and environmentally friendly practices. By financing green projects, reducing carbon footprints, and offering eco-friendly banking products, these initiatives contribute to a more sustainable and eco-friendly future while allowing customers to make socially responsible financial choices.

The Rise of Digital-First Banks

Digital-first banks, also known as neobanks or challenger banks, are on the ascent, fundamentally altering the banking landscape. These financial institutions operate solely in the digital realm, foregoing physical branches to reduce overhead costs. This enables them to provide customers with enticing interest rates, minimal fees, and a user-centric banking experience. Their streamlined account setup, intuitive mobile apps, and 24/7 accessibility have led to their rapid adoption. As digital-first banks continue to innovate and expand their services, they are poised to play a prominent role in shaping the future of online banking.

Enhanced User Experience

User experience (UX) is at the forefront of online banking’s evolution. Banks are investing heavily in user-friendly interfaces and mobile apps that offer seamless navigation, intuitive designs, and real-time access to accounts. This focus on UX ensures that customers can efficiently manage their finances while enjoying a user-centric experience. With rapid responses, real-time updates, and personalized financial services, online banking strives to provide a smooth, engaging, and secure environment. As technology advances, the commitment to enhancing user experiences remains a driving force in shaping the future of online banking.

Artificial Intelligence and Chatbots

Artificial intelligence (AI) and chatbots are revolutionizing customer service in online banking. These technologies provide quick, 24/7 responses to customer inquiries, assisting with account management and even offering financial advice. By analyzing data and customer behavior, AI-driven chatbots personalize interactions, making banking more convenient and accessible. They engage users in real-time, ensuring a responsive and informative experience. As AI and chatbot capabilities continue to grow, they play a pivotal role in shaping the future of online banking by providing efficient, effective, and user-friendly services.

Biometric Authentication

Biometric authentication is transforming online banking security. This method utilizes unique physical or behavioral traits, such as fingerprints, facial features, and voice patterns, to verify user identities. It offers a high level of security as these biometric data points are challenging to replicate, ensuring the integrity of online transactions. Biometric authentication enhances user experiences by eliminating the need for passwords or PINs, streamlining login processes, and providing a quick, secure, and user-friendly way to access accounts. With the emphasis on privacy and data protection, biometric authentication is poised to play a pivotal role in the future of online banking.

Personalized Financial Services

Personalized financial services are revolutionizing the online banking experience. By harnessing data analytics and artificial intelligence, banks offer tailored recommendations, investment guidance, and budgeting strategies based on individual spending patterns and financial goals. This level of customization empowers customers to make informed decisions and achieve their financial objectives. Personalized services also include real-time alerts, intuitive financial planning tools, and credit management guidance. As online banks continue to refine their personalization capabilities, customers can expect a more engaging, informative, and satisfying journey towards financial success. Personalized financial services are at the forefront of online banking’s evolution, delivering unparalleled value to customers.

Open Banking and Collaboration

Open banking is reshaping the financial industry by fostering collaboration between traditional banks and fintech innovators. It enables secure sharing of customer data with authorized third-party providers, promoting competition and innovation. Through open banking, customers can access a broader range of financial services within a unified platform, simplifying their financial management. This collaborative approach encourages healthy competition, improved customer experiences, and innovative solutions. Stringent security measures and data protection regulations ensure that customer data remains protected. As open banking gains momentum, it holds the potential to revolutionize the way we access and manage financial services in the digital era.

Blockchain Technology in Banking

Blockchain technology is revolutionizing the banking sector with its transparency, security, and efficiency. As a distributed ledger, it records transactions securely across a network of computers, making it virtually tamper-proof. This technology accelerates cross-border transactions, reduces costs, and streamlines complex processes. Smart contracts, self-executing agreements, automate various banking functions, such as loan origination and trade finance. Blockchain enhances identity verification, offering secure, user-controlled digital identities. It also facilitates the tokenization of assets, opening up new investment opportunities. By increasing transparency and security, blockchain is paving the way for a more efficient and secure future in banking.

Cybersecurity Measures

In the rapidly evolving landscape of online banking, robust cybersecurity measures are paramount. Banks employ advanced encryption methods, real-time monitoring, and threat detection systems to protect customer data and financial assets. These measures ensure the safety and integrity of online banking transactions and accounts, instilling trust and confidence in customers. As cyber threats continue to evolve, banks remain vigilant in adapting and strengthening their cybersecurity defenses to stay one step ahead of potential risks and attacks. Effective cybersecurity measures are essential in safeguarding the sensitive information and financial well-being of customers in the digital age.

Green Banking Initiatives

Green banking initiatives are reshaping the financial industry by promoting sustainability and eco-conscious practices. These initiatives involve investments in environmentally responsible projects, support for sustainable businesses, and eco-friendly banking products. Green banks aim to align financial services with environmentally aware consumers, encouraging socially responsible financial choices. By financing green projects, reducing carbon footprints, and offering sustainable banking options, these initiatives contribute to a more eco-friendly future. They enable customers to make financial decisions that are not only economically sound but also environmentally responsible, playing a vital role in addressing environmental challenges.

Conclusion

The future of online banking is a dynamic landscape, marked by innovations such as digital-first banks, AI-driven chatbots, biometric authentication, and blockchain technology. These advancements prioritize enhanced user experiences, robust cybersecurity measures, open banking collaborations, personalized financial services, and green banking initiatives. As the industry continues to evolve, it will be defined by a commitment to customer-centricity, security, sustainability, and technological progress, ultimately providing individuals with a more accessible, secure, and tailored approach to managing their finances.

FAQs

1. What is the role of blockchain in combating financial fraud in online banking?

Blockchain plays a crucial role in reducing financial fraud by providing an immutable and transparent ledger. It enhances security through cryptographic techniques, making it exceedingly difficult for unauthorized alterations of transaction records. This ensures the integrity of financial data and helps prevent fraudulent activities in online banking.

2. How do open banking initiatives protect customer data when sharing it with third-party providers?

Open banking initiatives prioritize data security by enforcing stringent regulations and protocols. Customer data is shared through secure Application Programming Interfaces (APIs) with explicit customer consent. Strong encryption and data protection measures are in place to safeguard sensitive information, ensuring privacy and security.

3. Can biometric authentication methods be fooled or hacked?

Biometric authentication methods like fingerprint recognition and facial recognition are highly secure due to their uniqueness and complexity. While it’s theoretically possible to spoof them, modern systems employ advanced technologies to detect and prevent such fraudulent attempts, making it extremely challenging for hackers to compromise biometric data.

4. How do green banking initiatives impact a bank’s profitability and operations?

Green banking initiatives can positively impact a bank’s profitability in the long term by attracting environmentally conscious customers and fostering sustainability in investments. While initial investments in eco-friendly practices may be required, the reduced environmental footprint and positive brand image can ultimately contribute to financial success.

5. What are the potential risks associated with AI-driven chatbots in online banking?

While AI-driven chatbots enhance user experiences, they can be vulnerable to hacking if not adequately secured. There’s also the risk of errors in responses or misinterpretation of customer queries. Banks must implement robust security measures and continuously monitor and update chatbot systems to mitigate these risks and ensure a seamless and secure customer interaction.